This article has also been published at the Business Science Institute: #Disruption and current #financialturmoil (impactknowledgebybusinessscienceinstitute.com)

For further discussion please get in touch with the authors.

Introduction

Is disruption hitting the banking sector? This question has become increasingly relevant as we see turmoil in financial institutions such as Credit Suisse. With many possible triggers for the occurrence of turmoil, in this essay, we will take a closer look at one: disruption itself. By placing focus on this singular aspect, we know that this complex situation requires a more in-depth analysis exceeding the scope of this essay. However, everything eventually is initiated by taking a first step.

Referring to our opening question of disruption in the banking industry, Bartz and Bärcher (2023) speculate how "Silicon Valley Brings Disruption to Global Finance”, in which they argue that “rising interest rates have plunged the financial markets into turbulence”. Regional U.S. Banks have already been facing bank-runs, while in Europe, most recent events show how some banks might also be on the brink. But is this the entire truth? With this essay, we set the foundation to provide more clarity and transparency, leveraging expert insights to get closer to the truth.

Challenges and impact

What might have started the most recent turmoil in the financial industry? Silicon Valley Bank (“SVB”) like many other banks, was confronted by “interest rate increases that many central banks are undertaking after the covid-19 pandemic” (Povey, 2023). At SVB, a combination of two bank-specific circumstances formed an unfortunate combination. On the one hand “SVB concentrated its deposit base in one sector, the start-up scene in Silicon Valley” (banking expert 3, 2023). When that sector faced a decline, as a result, many of SVB’s clients began simultaneously withdrawing deposits. On the other hand, management aimed to enhance profit by concentrating its investments on long-term bonds. Interest rates grew higher, decreasing the value of these bonds. Under normal circumstances, these losses end up unrealized, as bonds are held to maturity. However, because the deposit outflows were significant, the bank was required to sell the bonds and realize the losses. SVB thus required significant funds quickly, i.e., had “to raise more cash to compensate realized losses caused by the increasing withdrawal of deposits by investors” (banking expert 3, 2023). As LaCroix (2023) confirms this by stating that “rising interest rates caused the value of its bond investments to decline in value, which in turn generated losses when the bank had to liquidate investments to meet depositor withdrawal demands”. Selling government bonds at a much lower price than initially purchased may have triggered market psychology, in return causing concern among investors. McCabe and Mitchell (2023) argue that “investors have been on high alert for signs of contagion following the rapid collapse of California-based Silicon Valley Bank earlier this month”. This in turn “led to a sell-off in shares of banks around the world”.

As in the case for Credit Suisse, a ‘liquidity problem occurred’ instead: a nightmare for Credit Suisse had begun. Already before the ‘fall’ of Credit Suisse, the Swiss Banking regulator (FINMA), began their investigation on the back of the announcement of Credit Suisse’s chairman, where he stated that asset outflows are not considered as severe.

One significant event leading up to the ‘fall’, was the US Banking regulator Securities and Exchange Commission (SEC) calling Credit Suisse before the publication of its annual report was due (Ziady, 2023). As a result of this conversation, Credit Suisse had to postpone the publication and instead, release an according press release, which left a negative sentiment in the market. In addition, the Saudi National Bank, a key stakeholder of Credit Suisse, made its announcement of not further investing in Credit Suisse (Uppal, 2023).

“…This turmoil led for Credit Suisse to an accelerated asset outflow. The comment of the chair of the Saudi National Bank, not to buy more shares on regulatory grounds in Credit Suisse, coupled with the observed decrease in Credit Suisse’s stock price led to further outflows, especially in Asia-Pacific. Panic started to kick in that Credit Suisse, as system relevant bank might fail and ultimately cause another financial crisis…” (banking expert 1 and 2, 2023).

The market, predominantly investors, generally interpreted this as an additional loss of confidence, ignoring facts around regulatory caps that the Saudi National Bank was facing, i.e., according to the knowledge of our experts, no more than 10% of a single company may be held (banking expert 1, 2023). At this point, the momentum of market psychology took its course: negative headlines and perceptions by the market and investors significantly impacted the dynamics regarding market psychology.

The panic occurring in the market when losing confidence, may result in bank-runs. So-called market psychology, in which news about the stock market strongly influences the psychology of investors (Tetlock, 2007) is one potential trigger of bank-runs. As Tversky and Kahneman (1974) reason, the decision-making of individuals in uncertain situations is driven by heuristics as well as by cognitive biases. Heuristics is argued by Kahneman (2011) as being a research approach via progressive approximation of situations and problems. Steps are provisional, in which biases are represented as systemic errors, repeating themselves in predictable routines in specific situations. This coincides with Barberis and Thaler’s (2003) argument of behavioral finance focusing on the reflection of financial phenomena through models in which market agents are not always rational in their decision-making. Behavioral finance can be argued as the application of psychology to the discipline of finance (Pompian, 2006).

The overall tense macroenvironment that the banking sector is currently facing, has been accelerated by the bankruptcies of the SVB, Signature Bank, and various other banks in the US. This spillover to the European market, combined with an already extremely low level of confidence in Credit Suisse, resulted in an overnight challenge for the Credit Suisse. This panic which was created on the back of all events is considered the tipping point for Credit Suisse (banking expert 1, 2023).

The combination of these factors led to a massive loss in the value of the share price in a single day for Credit Suisse. As in finance the share price is viewed as a proxy for the health of a bank, the drop in price resulted in panic among Credit Suisse’s clients, who in return withdrew their assets. The outflows were so significant, as we understand, contrary to the statement made by the chairman, that there was a true risk of overnight insolvency. This action resulted in fear that the insolvency of the systemically important Credit Suisse would result in a global banking crisis, and therefore trigger the collapse of other banks. Additional pressure from the U.S., Great Britain, and France on Switzerland, its Swiss Confederation, and National Bank, required an immediate reaction. With the severity of time, an immediate solution had to be found over a weekend and be put in place before the Asian stock markets opened on Monday morning, to prevent further banks from being affected (banking expert 1, 2023). Evidently, this solution was the take-over of Credit Suisse by UBS.

Foundation

Taking all turns of events into close consideration, we predominantly question two things: what role did disruption play, and could a modular architecture have prevented this turmoil in the case of Credit Suisse?

Disruption itself. We consider disruption differently, as mentioned by Bartz and Bärcher (2023). Rather, we refer to disruption as “disruptive innovation” (Christensen, 1997). In this essay, we focus on the discourse grounded in different available viewpoints, supported by a feasible range of supporting arguments. Independent from this, we recall that “in today’s banking industry products and services are ‘good enough’ for the average consumers for which a performance surplus is created. An incumbent’s option to compete is by being fast, flexible, and responsive at a lower price” (Lettig et al., 2018, p.6). As the authors argue “modular versus interdependent architecture can provide an answer to disruption” (Lettig et al., 2018, p.3). “A traditional vertical forward integrated bank doing everything has no future because a firm cannot be excellent at everything and at the same time provide products and services to consumers at low cost while remaining agile” (Lettig et al., 2018, p. 5). New market entrants, who are viewed as being excellent at one element (i.e., standardized components with standardized interfaces) along the value chain, operate in an interconnected market and collaborate with other focused players. Consequently, “the whole becomes less efficient than the sum of its parts, and this a firm in providing one component very well being compatible through interfaces with other components from other component providers” (Lettig et al., 2018, p.5).

In the approach of modular architecture, as stated above, products, and services have the tendency to become ‘good enough’ for consumers, and thus, disrupters with specialized strategies hold a market reputation in performing single elements of a value chain at a higher standard. Why? Modular experts not only inhere to lower cost structures and therefore do not burden interdependence overhead, but moreover build up in-depth knowledge and expertise, allowing those disruptors to be closer to their consumer’s needs. What is the consequence? An increasing number of disrupters “enter the market and commoditization occurs” (Lettig et al., 2018, p.4). Versa, incumbents, as the authors argue (Lettig et al., 2018) must find ways in identifying new performance-defining components. Why? This is the sweet spot for a performing business. “The component in the value-stack that offers the functionality consumers care most and where the most profits can be made” (Lettig et al., 2018, p.4).

The fact that disruption forces incumbents to react to changes in competition, whether in the case of low-end or new market disruption, also implies that incumbents need to rethink their business model (Lettig et al., 2018). A question that remains unanswered is whether banks are taking the necessary steps to do this. Regarding the case of Credit Suisse, one of the areas to explore is the reason behind this failure. It is essential to identify the root cause behind the potential risk of failure for traditional banks as well as other incumbents. Hence, is there a correlation between this and disruption? With this question, we aim to open the gate for sound analyses and foster argumentative discourse.

Method

This essay provides a possible explanation of the current financial turmoil, presents our thoughts and opinions via discourse, as well as a possible solution approach. This all serves as a foundation to inspire future research.

Our desktop research is composed of professional articles and blogs providing an initial overview of the situation. We corroborated the desktop research by expert interviews to identify the context of Credit Suisse’s turmoil. Furthermore, it is an efficient method to gather data. Experts provide practical know-how which can hardly be replicated by other forms of research. Through the interviewing process, data can quickly lead to qualitative results (Bogner et al., 2009, p. 1). Therefore, both together gives an according point of view regarding the turmoil. Because the current situation is timely and delicate, our expert interviewees want to be referenced anonymously.

Possible solution approach

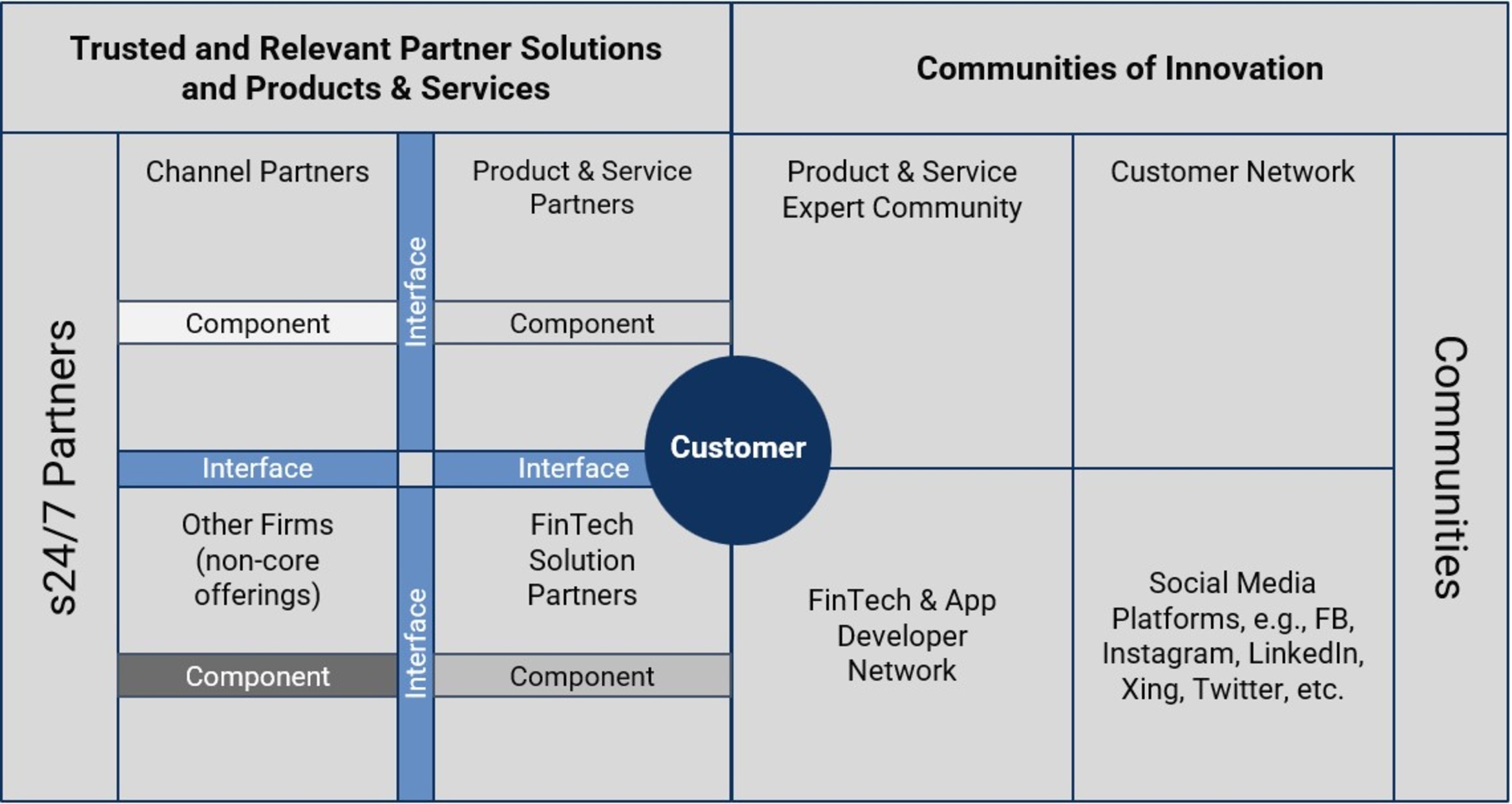

One approach to prevent such bank failure could be an ecosystem or platform business model strategy with modular standardized components and interfaces, as depicted in a “Showcase s24/7” (Lettig et al., 2018, p.13). There, components, possibly as Software-as-a-Service, operate as independent and decoupled business segments, based on defining core and non-core products and services. Note that decoupling here refers to the reduction of dependencies amongst products and services as well as markets. Therefore, when being hit by turmoil, only one or a few components might be affected, while others remain unaffected due to the independent nature of the platform business model or ecosystem strategy. This business model thus has the potential to mitigate and reduce risk and overall failure over time. In the case of Credit Suisse, as it seems, its pipeline business model, being defined as traditional and forward integrated, is based on an interdependent architecture. Although, we are not in the position to claim that no attempts were made for a change in the business model as such by Credit Suisse. Nonetheless, the question remains, if so, was it done coherently?

Generally, success in any business is defined by the degree of monetization and willingness to pay by consumers. The monetization of platforms comprises four venues:

-

‘transaction cut’ a fee is charged to component providers for facilitating transactions

-

‘pay for access’ charging actors on the platform for lead generation, i.e., “charging the side that needs the other side more” (Lettig, et al., 2018, p. 17)

-

‘pay for attention’ charging for matching, and

-

‘pay for tools’ charging for upgrades or better tools

The authors (Lettig et al., 2018) explain that “even though s24/7, in offering to various component providers, the platform must carry overhead costs, which can be absorbed through extracting value by adopting either of the four forms of monetization” (p. 17). A “platform only owns those resources that are inimitable by component providers” (p. 18). Hence, the majority of components are decoupled from the platform and thus detached from possible turmoil faced by other component providers. This corroborates the previous argument, that a platform or ecosystem could protect from turmoil and has the potential to mitigate risk.

Conclusion

We presented the current situation of turmoil with an explanation of the possible effects on Credit Suisse’s challenges, which resulted in the takeover by UBS. We argued about disruption being one aspect of possible root cause and presented a solution approach via the “Showcase s24/7”, i.e., a modular platform and ecosystem business model.

This situation resulting in turmoil requires a deeper understanding of what happened at its root cause as well as a thorough analysis. We do not claim to know the precise answer, yet, but want to provide food for thought, arguments, and discourse. It is in our interest to understand whether a correlation between disruption and the current turmoil exists and whether the “Showcase s24/7” as a modular business model or an ecosystem, is a valid approach to mitigate risks.

We summarize this short discourse with Christensen’s argument that “an organization cannot disrupt itself” (2013, p. 198). Sadly, this concludes that dis-integration for forward-integrated incumbents will continuously present a challenge. Why? Because organizations “can only naturally prioritize innovations that promise improved profit margins relative to their current cost structure” (p. 198). And ultimately, the solution found with the takeover of Credit Suisse by UBS, does not resolve the situation completely but rather makes UBS “even bigger than too big to fail” (WirtschaftsWoche, 2023).

Finally, we ask again, is disruption hitting the banking sector? We have started this discussion based on a set of arguments for potential mechanisms with their derivation and thoughts for a possible solution approach. With this contribution, we would like to foster further research, analysis, and discourse regarding this complex situation.

Future Research

With our essay, we have addressed the surface of the most recent market developments. To go beyond, aspects to be explored are

-

The understanding to which extent a platform business model or ecosystem strategy is affected in the occurrence of a loss in confidence and its correlation to market psychology

-

The different roles banks play (e.g., orchestration) and their effect on interdependencies of structures as well as a degree of risk mitigation

-

The complexity of risks (e.g., legacy structures) connected to transformation, which prevents banks from realizing new business models

All those present interesting avenues for future research, as market psychology is a factor whose influence is not to be underestimated.

A concluding aspect, specifically in the case of Credit Suisse, which requires additional research, is with UBS now being considered bigger than too big to fail (WirtschaftsWoche, 2023), how can this challenge be solved? Since “an organization cannot disrupt itself” (Christensen, 2013, p. 198), a yet undefined alley of solutions has to be explored. Initial thoughts comprise a transformational organizational approach which introduces an ecosystem or platform business model for Credit Suisse and/or UBS or the development of a new start-up, to reduce interdependencies and disrupt the traditional ways of banking.

References

Banking expert 1 (2023) What happened at the downfall of Credit Suisse [Interview], AdEx Partners with S Lettig, 22nd March 2023. Zürich.

Banking expert 2 (2023) What happened at the downfall of Credit Suisse [Interview], AdEx Partners with S Lettig, 22nd March 2023. Zürich.

Banking expert 3 (2023) What happened at the downfall of Silicon Valley Bank and how did it affect the downfall of Credit Suisse and what happened at the downfall of Credit Suisse [Interview], AdEx Partners with S Lettig, 24th March 2023. Zürich.

Barberis, N., & Thaler, R. (2003). A survey of behavioral finance. In G. M. Constantinides, M. Harris, & R. M. Stulz (Eds.), Handbook of the economics of finance (pp. 051–1121). Elsevier.

Bartz, T. and Brächer, M. (2023) Silicon Valley Brings Disruption to Global Finance. Spiegel International, 17 March 2023. Available at: https://www.spiegel.de/international/business/svb-s-european-shockwaves-silicon-valley-brings-disruption-to-global-finance-a-5ec8b93d-b3be-44d7-9968-8a54d83051eb

Bogner, A., Littig, B., & Menz, W. (2009). Introduction: Expert interviews—An introduction to a new methodological debate. Interviewing experts, 1-13.

Christensen, C.M. (1997) The Innovator’s Dilemma. When New Technologies Cause Great Firms to Fail. Harvard Business Review Press.

Kahneman, D. (2011). Thinking, fast and slow. New York: Penguin.

LaCroix, K.M. (2023) What Does the Failure of Silicon Valley Bank Mean? The D&O Diary, 12 March, 2023. Available at: https://www.dandodiary.com/2023/03/articles/uncategorized/what-does-the-failure-of-silicon-valley-bank-mean/

Lettig, S., Bundi, D. and, Ramirez, G. (2018) Modular Business Architecture as Banking Use Case. Disruption Disciples Whitepaper #01. Available at: https://www.disruptiondisciples.org/wp-content/uploads/2019/04/Disruption_Disciples_Whitepaper.pdf

McCabe, C. and Mitchell, J. (2023) Why Is Credit Suisse in Trouble? The Banking Turmoil Explained. The Wall Street Journal, 20 March, 2023. Available at: https://www.wsj.com/articles/why-is-credit-suisse-in-trouble-the-banking-turmoil-explained-6f8ddb5b

Pompian, M. (2011) Behavioral Finance and Wealth Management. 1st edn. New Jersey: Wiley.

Povey, O. (2023) Are the collapses of Credit Suisse and Silicon Valley Bank connected? Diaro AS, 16 March, 2023. Available at: https://en.as.com/latest_news/are-the-collapses-of-credit-suisse-and-silicon-valley-bank-connected-n/

Schnaas, D. (2023) Wir sitzen im Kartenhaus. Interview, WirtschafsWoche, 22 March, 2023. Available at: https://www.wiwo.de/unternehmen/energie/banken-und-finanzkrise-wir-sitzen-im-kartenhaus/29050674.html

Tetlock, P. C. (2007) Giving content to investor sentiment: The role of media in the stock market. The Journal of finance, 62(3), pp. 1139-1168.

Tversky, A., and Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185 (4157), 1124–1131.

Uppal, R. (2023) Credit Suisse's biggest backer says can't put up more cash; share down by a fifth. Reuters, 15 March, 2023. Available at: https://www.reuters.com/business/finance/credit-suisses-saudi-backer-happy-with-transformation-plan-doesnt-think-extra-2023-03-15/

Ziady, H. (2023) Credit Suisse delays annual report after 'late call' from the SEC. CNN Business, 9 March, 2023. Available at: https://edition.cnn.com/2023/03/09/investing/credit-suisse-annual-report-sec/index.html